Global warming is the gradual increase in temperature of Earth’s atmosphere due to greenhouse gases (GHG) such as carbon dioxide, methane, and nitrous oxide. In recent years, global warming is believed to be caused by human activity. Our species evolved to be dependent on ever increasing quantities of cheap energy, and this has led us into a downward cycle that can cause negative consequences to earth. This is what many have identified as a Climate Crisis.

So, what can be done about the climate crisis? There are a few options. Some voices promote the idea that countries like China and India could use less resources to achieve their current level of development and leave more resources for other countries to develop sustainably. This is unlikely since it would require a sacrifice on the part of individuals in these nations. Another option is to increase the capacity of sustainable energy production. This will certainly help with our sustainability problem, but at a cost. It means that we must develop new technology or find cheaper ways of producing clean energy from sources other than coal, oil and gas. Looking at the previous examples, we realize that on the surface the climate crisis looks like a zero sum game to many people. However, when we investigate this issue deeper, it turns out to be more complex.

The first step in addressing the climate crisis is to identify the various forces that will impact GHG emissions and climate change. We believe there are three major forces in play:

1) GDP

Gross Domestic Product (GDP) has been one of the most important economic metrics for evaluating countries economic annual success. GDP growth as a goal makes economic activity focused on increasing activities in goods and services markets. This can push economic activity to pursue short term profit tactics such as pursuing the lowest costs for materials and energy, as well as less weight on societal or environmental impacts of the economic activities. This is a driving force as GDP metrics do not take into account climate impacts. In short, if GDP takes into account climate impact it will be a positive reinforcement mechanism for more sustainable economic growth.

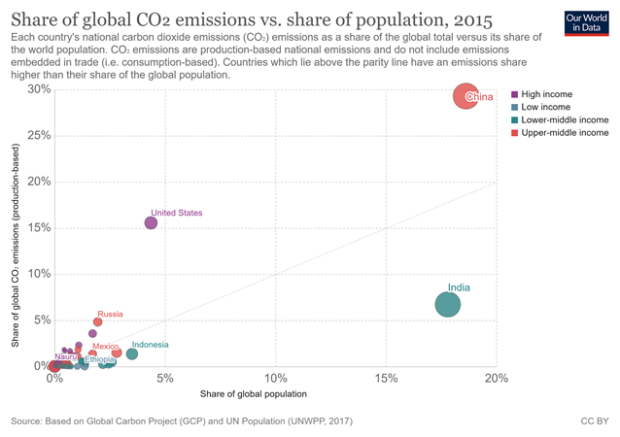

2) Population

Growth in population is generally related to consumption of goods and services. The more the population would grow, their consumption will grow, given a flat or positive change consumption per capita. Consequently, the environmental impact of population change is a driving force in the climate change challenge. Population growth that is combined with optimized consumption would be ideal for a positive climate impact.

3) The cost of energy

The cost of energy is a determining factor in consumption quantities, the lower the energy costs, the more attractive energy consumption becomes. Energy costs are also a driving factor in the energy consumption by type of energy source, hence the climate impact of energy consumption. The variation of energy costs has second degree effects on the climate challenge. Below we show how gasoline prices changed in the past eight decades in the US, while the gasoline cost varied upward and downward, it is important to note that the energy mix, consumption, as well as emissions also GHG varied accordingly.

For these three forces to work together towards a lower carbon future there has to be an ultimate collaboration between countries, businesses, and individuals to ensure an equitable and just transition. A smooth transition would minimize risks to society, countries, as well as special interest groups. We would call this a “beautiful climate transition”, this transition would be inclusive of entities at risk, such as industries at risk as they rely on activities that impose climate risks. These entities would include oil and gas industries, and heavy industries like metals and some aspects of manufacturing. There are exciting opportunities for such industries in the fields of energy generation[1] as well as opportunities in being key players in deflationary energy cost disruption[2]. It is imperative that these opportunities should be incentivized by both governments and by private entities in order for them to materialize.

The upside for these opportunities outweigh the risk associated with costs for implementation. The core message here is that technology itself would not be the only important force for a climate transition. It is important for the public to understand the magnitude of the contribution of the “at risk” industries when focusing on the climate transition. The oil and gas industry is a 3.3 Trillion dollar global industry[3] that contributes 8% to the US GDP[4] and petroleum exports can contribute up to 42 % of GDP in some countries[5] that heavily rely on oil as a source of income. Industries including manufacturing, constitutes a large GDP percentage[6] of the biggest economies in the world like China (40%), India (23%) and the US (19%). In addition, the electricity for power generation that back these industries, and other human activities, are generated by fossil fuels[7]. For example, as a reality check, we show the share of electricity production from fossil fuel by country below the majority of the world is at 60% or more.

The fossil fuel power generation is a 125 billion dollar industry[8] that is expected to have considerable investments for the next decade. In addition, fossil fuel power generation still constitutes more than 63.3% of global power generation[9]. It would be foolish to think that the oil and gas industries will not play a fundamental role in the energy transition. In addition, the demand for energy use is expected to increase because of the increase in human activity[10] and consumption[11]. This increase is expected to continue in the future which poses important questions on how these demands will be met in the future and how the fossil fuel based industries will transform to satisfy these demands while accommodating a low carbon transition. As a reality check, we highlight below the investments of fossil fuels in 2018 and the projected investments in the next 5 to 10 years, the staggering numbers reach 1 Trillion dollars at a point.

A big chunk of this transition challenge is not technology driven but will be rather driven by other important forces. Two of these important forces that would help guide the transition to low carbon energy are: Regulation and Taxes

Regulation

Regulations targeting GHG emissions have been getting more and more stringent over the past few decades. For example, in the field of vehicle emissions, the European Union[12] and China[13] are progressing rapidly towards lower emissions standards. If the world chooses to pursue a lower GHG path in the next few decades, regulations will be one of the tools that would drive this transition. For example, government policy can dictate what is permitted and what is not, this includes GHG emitting equipment, buildings, construction, manufacturing, and transport. A ban on internal combustion engines (ICE) sales[14] or single use plastics[15] is a prime example of the use of regulation to drive a low carbon transition. It will not be surprising that such regulatory policy tools will be used to shape the low carbon transition in other ways. For example, regulation can become more robust in allowing low carbon pathways to accelerate further than other pathways. This can be through regulatory incentives to low carbon technologies such as allowing faster deployment. It can also be through more resource allocations to approvals and faster processing for low carbon related activities such as hydropower, SMR, Recycling, Waste to Fuel.

Taxes

Carbon pricing, carbon taxes, and carbon accounting, are all buzz words being used by many voices to highlight the need to include GHG impact in the economic formulas of human activities. The key issue that faces this complex challenge is accurately quantifying the economic impact of GHG across the board. It is also challenging to determine how including GHG in economic formulas disproportionately affects different locations around the world. What adds to this complexity is the uncertainty in forecasting the behavioral feedback to include GHG impacts the economy of human day to day activity. Some groups will have positive reactions while other groups will not react. It is key for decision makers to remember that using the economy to change human behavior is a balancing act where swift versus abrupt changes can trigger either blaring success or catastrophic failure.

The two above mentioned forces as well as the factors we explored earlier will play a key role in the low carbon transformation along with technology, because it is not only about technology. It will be important to keep an eye on this over the next few years.

Reference

[1] “Climate Change & A Geothermal Future – DataDrivenInvestor.” 23 Sep. 2020, https://medium.datadriveninvestor.com/climate-change-and-a-geothermal-future-b202c133024e. Accessed 13 Mar. 2021.

[2] “Addressing Climate Change: A close brief look at the future of small ….” https://medium.com/@7asabala/addressing-climate-change-a-close-brief-look-at-the-future-of-small-nuclear-energy-part-ii-b61f325fbe80. Accessed 13 Mar. 2021.

[3] “What Percentage of the Global Economy Is the Oil and Gas Drilling ….” 15 Feb. 2020, https://www.investopedia.com/ask/answers/030915/what-percentage-global-economy-comprised-oil-gas-drilling-sector.asp. Accessed 15 Mar. 2021.

[4] “Oil & Natural Gas Contribution to U.S. Economy Fact She – API.” https://www.api.org/news-policy-and-issues/taxes/oil-and-natural-gas-contribution-to-us-economy-fact-sheet. Accessed 17 Mar. 2021.

[5] “Saudi Arabia – Forbes.” https://www.forbes.com/places/saudi-arabia/. Accessed 15 Mar. 2021.

[6] “GDP – composition, by sector of origin – The World Factbook – CIA.” https://www.cia.gov/the-world-factbook/field/gdp-composition-by-sector-of-origin. Accessed 17 Mar. 2021.

[7] “Frequently Asked Questions (FAQs) – U.S. Energy Information … – EIA.” 5 Mar. 2021, https://www.eia.gov/tools/faqs/faq.php?id=427&t=3. Accessed 17 Mar. 2021.

[8] “Energy investment by scenario, 2025-2030 – Charts – Data … – IEA.” 28 Nov. 2019, https://www.iea.org/data-and-statistics/charts/energy-investment-by-scenario-2025-2030. Accessed 17 Mar. 2021.

[9] “Electricity Mix – Our World in Data.” https://ourworldindata.org/electricity-mix. Accessed 17 Mar. 2021.

[10] “EIA projects nearly 50% increase in world energy usage by 2050 ….” 24 Sep. 2019, https://www.eia.gov/todayinenergy/detail.php?id=41433. Accessed 17 Mar. 2021.

[11] “Global Material Resources Outlook to 2060 – OECD.” https://www.oecd.org/environment/waste/highlights-global-material-resources-outlook-to-2060.pdf. Accessed 17 Mar. 2021.

[12] “CO₂ emission performance standards for cars and vans (2020 ….” https://ec.europa.eu/clima/policies/transport/vehicles/regulation_en. Accessed 27 Mar. 2021.

[13] “China: Light-duty: Emissions | Transport Policy – TransportPolicy.net.” https://www.transportpolicy.net/standard/china-light-duty-emissions/. Accessed 27 Mar. 2021.

[14] “Britain’s Accelerated ICE Vehicle Sales Ban Aims To Speed CO2 ….” 18 Nov. 2020, https://www.forbes.com/sites/neilwinton/2020/11/18/britains-accelerated-ice-vehicle-sales-ban-aims-to-speed-co2-progress-with-unintended-consequences/. Accessed 27 Mar. 2021.

[15] “Which countries have bans on single-use plastics? | World ….” 26 Oct. 2020, https://www.weforum.org/agenda/2020/10/canada-bans-single-use-plastics/. Accessed 27 Mar. 2021.